-

Itália

Itália

International distribution agreements | Key Clauses and Lessons learned from the history of Nike

30 de Março, 2026

- Contratos

- Distribuição

- Propriedade intelectual

- Marca registada e patentes

Summary

Phil Knight, the founder of Nike, imported the Japanese brand Onitsuka Tiger into the US market in 1964 and quickly gained a 70% share. When Knight learned Onitsuka was looking for another distributor, he created the Nike brand. This led to two lawsuits between the two companies, but Nike eventually won and became the most successful sportswear brand in the world. This article looks at the lessons to be learned from the dispute, such as how to negotiate an international distribution agreement, contractual exclusivity, minimum turnover clauses, duration of the contract, ownership of trademarks, dispute resolution clauses, and more.

What I talk about in this article

- The Blue Ribbon vs. Onitsuka Tiger dispute and the birth of Nike

- How to negotiate an international distribution agreement

- Contractual exclusivity in a commercial distribution agreement

- Minimum Turnover clauses in distribution contracts

- Duration of the contract and the notice period for termination

- Ownership of trademarks in commercial distribution contracts

- The importance of mediation in international commercial distribution agreements

- Dispute resolution clauses in international contracts

- How we can help you

The Blue Ribbon vs Onitsuka Tiger dispute and the birth of Nike

Why is the most famous sportswear brand in the world Nike and not Onitsuka Tiger?

Shoe Dog is the biography of the creator of Nike, Phil Knight: for lovers of the genre, but not only, the book is really very good and I recommend reading it.

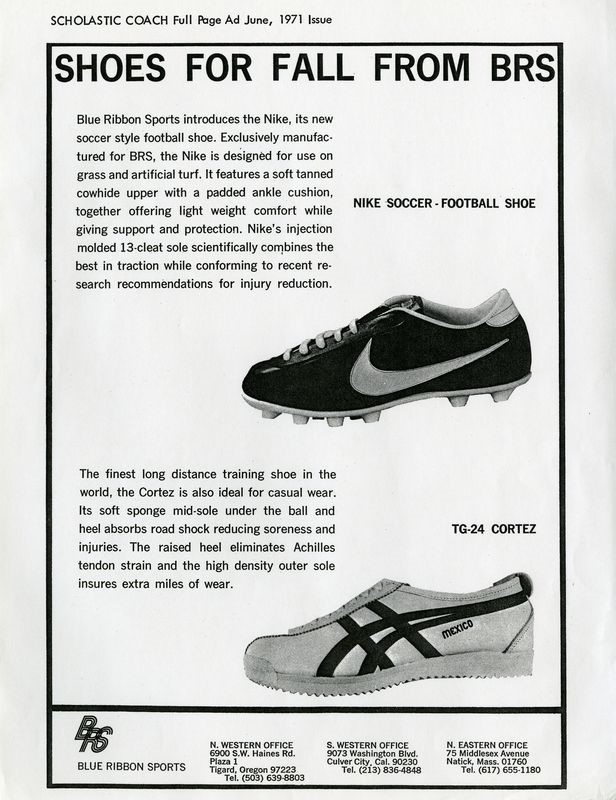

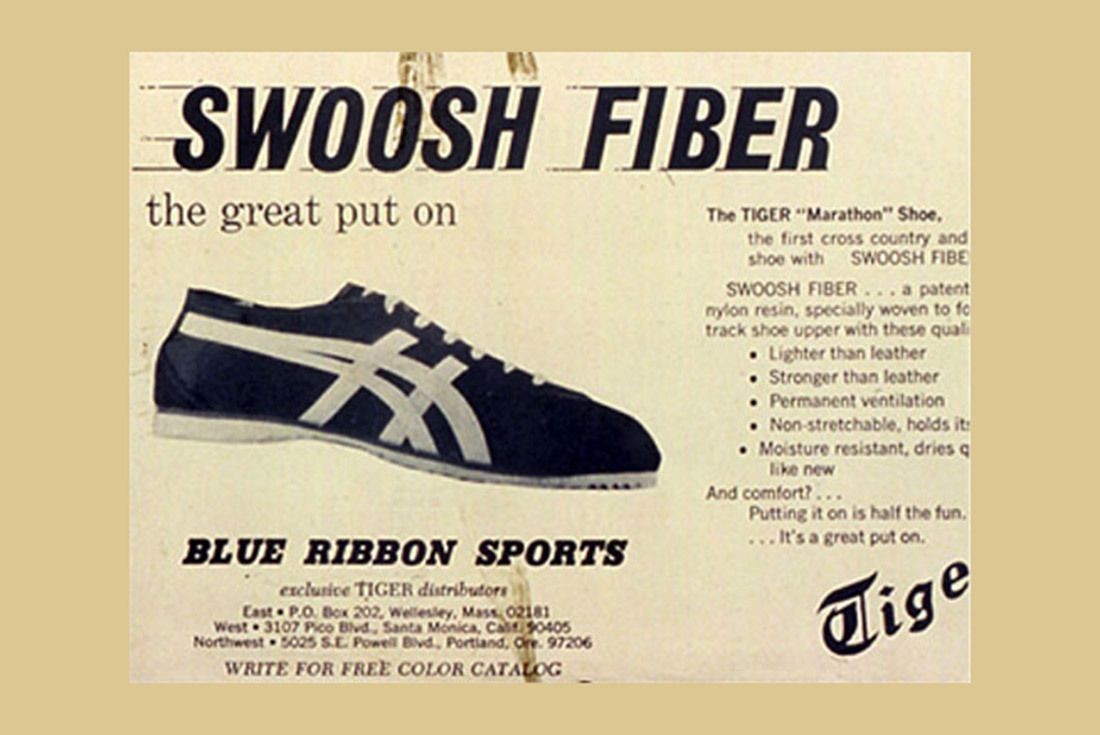

Moved by his passion for running and intuition that there was a space in the American athletic shoe market, at the time dominated by Adidas, Knight was the first, in 1964, to import into the U.S. a brand of Japanese athletic shoes, Onitsuka Tiger, coming to conquer in 6 years a 70% share of the market.

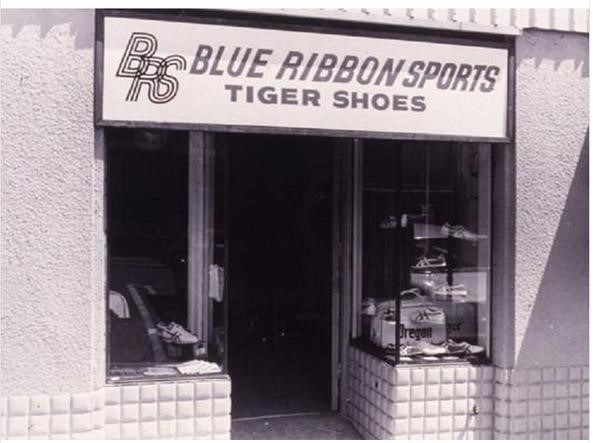

The company founded by Knight and his former college track coach, Bill Bowerman, was called Blue Ribbon Sports.

The business relationship between Blue Ribbon-Nike and the Japanese manufacturer Onitsuka Tiger was, from the beginning, very turbulent, despite the fact that sales of the shoes in the U.S. were going very well and the prospects for growth were positive.

When, shortly after having renewed the contract with the Japanese manufacturer, Knight learned that Onitsuka was looking for another distributor in the U.S., fearing to be cut out of the market, he decided to look for another supplier in Japan and create his own brand, Nike.

Upon learning of the Nike project, the Japanese manufacturer challenged Blue Ribbon for violation of the non-competition agreement, which prohibited the distributor from importing other products manufactured in Japan, declaring the immediate termination of the agreement.

In turn, Blue Ribbon argued that the breach would be Onitsuka Tiger’s, which had started meeting other potential distributors when the contract was still in force and the business was very positive.

This resulted in two lawsuits, one in Japan and one in the U.S., which could have put a premature end to Nike’s history.

Fortunately (for Nike) the American judge ruled in favor of the distributor and the dispute was closed with a settlement: Nike thus began the journey that would lead it 15 years later to become the most important sporting goods brand in the world.

Let’s see what Nike’s history teaches us and what mistakes should be avoided in an international distribution contract.

How to negotiate an international commercial distribution agreement

In his biography, Knight writes that he soon regretted tying the future of his company to a hastily written, few-line commercial agreement at the end of a meeting to negotiate the renewal of the distribution contract.

What did this agreement contain?

The agreement only provided for the renewal of Blue Ribbon’s right to distribute products exclusively in the USA for another three years.

It often happens that international distribution contracts are entrusted to verbal agreements or very simple contracts of short duration: the explanation that is usually given is that in this way it is possible to test the commercial relationship, without binding too much to the counterpart.

This way of doing business, though, is wrong and dangerous: the contract should not be seen as a burden or a constraint, but as a guarantee of the rights of both parties. Not concluding a written contract, or doing so in a very hasty way, means leaving without clear agreements fundamental elements of the future relationship, such as those that led to the dispute between Blue Ribbon and Onitsuka Tiger: commercial targets, investments, ownership of brands.

If the contract is also international, the need to draw up a complete and balanced agreement is even stronger, given that in the absence of agreements between the parties, or as a supplement to these agreements, a law with which one of the parties is unfamiliar is applied, which is generally the law of the country where the distributor is based.

Even if you are not in the Blue Ribbon situation, where it was an agreement on which the very existence of the company depended, international contracts should be discussed and negotiated with the help of an expert lawyer who knows the law applicable to the agreement and can help the entrepreneur to identify and negotiate the important clauses of the contract.

Territorial exclusivity, commercial objectives and minimum turnover targets

The first reason for conflict between Blue Ribbon and Onitsuka Tiger was the evaluation of sales trends in the US market.

Onitsuka argued that the turnover was lower than the potential of the U.S. market, while according to Blue Ribbon the sales trend was very positive, since up to that moment it had doubled every year the turnover, conquering an important share of the market sector.

When Blue Ribbon learned that Onituska was evaluating other candidates for the distribution of its products in the USA and fearing to be soon out of the market, Blue Ribbon prepared the Nike brand as Plan B: when this was discovered by the Japanese manufacturer, the situation precipitated and led to a legal dispute between the parties.

The dispute could perhaps have been avoided if the parties had agreed upon commercial targets and the contract had included a fairly standard clause in exclusive distribution agreements, i.e. a minimum sales target on the part of the distributor.

In an exclusive distribution agreement, the manufacturer grants the distributor strong territorial protection against the investments the distributor makes to develop the assigned market.

In order to balance the concession of exclusivity, it is normal for the producer to ask the distributor for the so-called Guaranteed Minimum Turnover or Minimum Target, which must be reached by the distributor every year in order to maintain the privileged status granted to him.

If the Minimum Target is not reached, the contract generally provides that the manufacturer has the right to withdraw from the contract (in the case of an open-ended agreement) or not to renew the agreement (if the contract is for a fixed term) or to revoke or restrict the territorial exclusivity.

In the contract between Blue Ribbon and Onitsuka Tiger, the agreement did not foresee any targets (and in fact the parties disagreed when evaluating the distributor’s results) and had just been renewed for three years: how can minimum turnover targets be foreseen in a multi-year contract?

In the absence of reliable data, the parties often rely on predetermined percentage increase mechanisms: +10% the second year, + 30% the third, + 50% the fourth, and so on.

The problem with this automatism is that the targets are agreed without having available the real data on the future trend of product sales, competitors’ sales and the market in general, and can therefore be very distant from the distributor’s current sales possibilities.

For example, challenging the distributor for not meeting the second or third year’s target in a recessionary economy would certainly be a questionable decision and a likely source of disagreement.

It would be better to have a clause for consensually setting targets from year to year, stipulating that targets will be agreed between the parties in the light of sales performance in the preceding months, with some advance notice before the end of the current year. In the event of failure to agree on the new target, the contract may provide for the previous year’s target to be applied, or for the parties to have the right to withdraw, subject to a certain period of notice.

It should be remembered, on the other hand, that the target can also be used as an incentive for the distributor: it can be provided, for example, that if a certain turnover is achieved, this will enable the agreement to be renewed, or territorial exclusivity to be extended, or certain commercial compensation to be obtained for the following year.

A final recommendation is to correctly manage the minimum target clause, if present in the contract: it often happens that the manufacturer disputes the failure to reach the target for a certain year, after a long period in which the annual targets had not been reached, or had not been updated, without any consequences.

In such cases, it is possible that the distributor claims that there has been an implicit waiver of this contractual protection and therefore that the withdrawal is not valid: to avoid disputes on this subject, it is advisable to expressly provide in the Minimum Target clause that the failure to challenge the failure to reach the target for a certain period does not mean that the right to activate the clause in the future is waived.

The notice period for terminating an international distribution contract

The other dispute between the parties was the violation of a non-compete agreement: the sale of the Nike brand by Blue Ribbon, when the contract prohibited the sale of other shoes manufactured in Japan.

Onitsuka Tiger claimed that Blue Ribbon had breached the non-compete agreement, while the distributor believed it had no other option, given the manufacturer’s imminent decision to terminate the agreement.

This type of dispute can be avoided by clearly setting a notice period for termination (or non-renewal): this period has the fundamental function of allowing the parties to prepare for the termination of the relationship and to organize their activities after the termination.

In particular, in order to avoid misunderstandings such as the one that arose between Blue Ribbon and Onitsuka Tiger, it can be foreseen that during this period the parties will be able to make contact with other potential distributors and producers, and that this does not violate the obligations of exclusivity and non-competition.

In the case of Blue Ribbon, in fact, the distributor had gone a step beyond the mere search for another supplier, since it had started to sell Nike products while the contract with Onitsuka was still valid: this behavior represents a serious breach of an exclusivity agreement.

A particular aspect to consider regarding the notice period is the duration: how long does the notice period have to be to be considered fair? In the case of long-standing business relationships, it is important to give the other party sufficient time to reposition themselves in the marketplace, looking for alternative distributors or suppliers, or (as in the case of Blue Ribbon/Nike) to create and launch their own brand.

The other element to be taken into account, when communicating the termination, is that the notice must be such as to allow the distributor to amortize the investments made to meet its obligations during the contract; in the case of Blue Ribbon, the distributor, at the express request of the manufacturer, had opened a series of mono-brand stores both on the West and East Coast of the U.S.A..

A closure of the contract shortly after its renewal and with too short a notice would not have allowed the distributor to reorganize the sales network with a replacement product, forcing the closure of the stores that had sold the Japanese shoes up to that moment.

Generally, it is advisable to provide for a notice period for withdrawal of at least 6 months, but in international distribution contracts, attention should be paid, in addition to the investments made by the parties, to any specific provisions of the law applicable to the contract (here, for example, an in-depth analysis for sudden termination of contracts in France) or to case law on the subject of withdrawal from commercial relations (in some cases, the term considered appropriate for a long-term sales concession contract can reach 24 months).

Finally, it is normal that at the time of closing the contract, the distributor is still in possession of stocks of products: this can be problematic, for example because the distributor usually wishes to liquidate the stock (flash sales or sales through web channels with strong discounts) and this can go against the commercial policies of the manufacturer and new distributors.

In order to avoid this type of situation, a clause that can be included in the distribution contract is that relating to the producer’s right to repurchase existing stock at the end of the contract, already setting the repurchase price (for example, equal to the sale price to the distributor for products of the current season, with a 30% discount for products of the previous season and with a higher discount for products sold more than 24 months previously).

Trademark Ownership in an International Distribution Agreement

During the course of the distribution relationship, Blue Ribbon had created a new type of sole for running shoes and coined the trademarks Cortez and Boston for the top models of the collection, which had been very successful among the public, gaining great popularity: at the end of the contract, both parties claimed ownership of the trademarks.

Situations of this kind frequently occur in international distribution relationships: the distributor registers the manufacturer’s trademark in the country in which it operates, in order to prevent competitors from doing so and to be able to protect the trademark in the case of the sale of counterfeit products; or it happens that the distributor, as in the dispute we are discussing, collaborates in the creation of new trademarks intended for its market.

At the end of the relationship, in the absence of a clear agreement between the parties, a dispute can arise like the one in the Nike case: who is the owner, producer or distributor?

In order to avoid misunderstandings, the first advice is to register the trademark in all the countries in which the products are distributed, and not only: in the case of China, for example, it is advisable to register it anyway, in order to prevent third parties in bad faith from taking the trademark (for further information see this post on Legalmondo).

It is also advisable to include in the distribution contract a clause prohibiting the distributor from registering the trademark (or similar trademarks) in the country in which it operates, with express provision for the manufacturer’s right to ask for its transfer should this occur.

Such a clause would have prevented the dispute between Blue Ribbon and Onitsuka Tiger from arising.

The facts we are recounting are dated 1976: today, in addition to clarifying the ownership of the trademark and the methods of use by the distributor and its sales network, it is advisable that the contract also regulates the use of the trademark and the distinctive signs of the manufacturer on communication channels, in particular social media.

It is advisable to clearly stipulate that the manufacturer is the owner of the social media profiles, of the content that is created, and of the data generated by the sales, marketing and communication activity in the country in which the distributor operates, who only has the license to use them, in accordance with the owner’s instructions.

In addition, it is a good idea for the agreement to establish how the brand will be used and the communication and sales promotion policies in the market, to avoid initiatives that may have negative or counterproductive effects.

The clause can also be reinforced with the provision of contractual penalties in the event that, at the end of the agreement, the distributor refuses to transfer control of the digital channels and data generated in the course of business.

Mediation in international commercial distribution contracts

Another interesting point offered by the Blue Ribbon vs. Onitsuka Tiger case is linked to the management of conflicts in international distribution relationships: situations such as the one we have seen can be effectively resolved through the use of mediation.

This is an attempt to reconcile the dispute, entrusted to a specialized body or mediator, with the aim of finding an amicable agreement that avoids judicial action.

Mediation can be provided for in the contract as a first step, before the eventual lawsuit or arbitration, or it can be initiated voluntarily within a judicial or arbitration procedure already in progress.

The advantages are many: the main one is the possibility to find a commercial solution that allows the continuation of the relationship, instead of just looking for ways for the termination of the commercial relationship between the parties.

Another interesting aspect of mediation is that of overcoming personal conflicts: in the case of Blue Ribbon vs. Onitsuka, for example, a decisive element in the escalation of problems between the parties was the difficult personal relationship between the CEO of Blue Ribbon and the Export manager of the Japanese manufacturer, aggravated by strong cultural differences.

The process of mediation introduces a third figure, able to dialogue with the parts and to guide them to look for solutions of mutual interest, that can be decisive to overcome the communication problems or the personal hostilities.

For those interested in the topic, we refer to this post on Legalmondo and to the replay of a recent webinar on mediation of international conflicts.

Dispute resolution clauses in international distribution agreements

The dispute between Blue Ribbon and Onitsuka Tiger led the parties to initiate two parallel lawsuits, one in the US (initiated by the distributor) and one in Japan (rooted by the manufacturer).

This was possible because the contract did not expressly foresee how any future disputes would be resolved, thus generating a very complicated situation, moreover on two judicial fronts in different countries.

The clauses that establish which law applies to a contract and how disputes are to be resolved are known as “midnight clauses“, because they are often the last clauses in the contract, negotiated late at night.

They are, in fact, very important clauses, which must be defined in a conscious way, to avoid solutions that are ineffective or counterproductive.

How we can help you

The construction of an international commercial distribution agreement is an important investment, because it sets the rules of the relationship between the parties for the future and provides them with the tools to manage all the situations that will be created in the future collaboration.

It is essential not only to negotiate and conclude a correct, complete and balanced agreement, but also to know how to manage it over the years, especially when situations of conflict arise.

Legalmondo offers the possibility to work with lawyers experienced in international commercial distribution in more than 60 countries: write us your needs.

Establishing a joint venture in Saudi Arabia can be an extremely attractive option for foreign investors. It provides access to local expertise, market knowledge, business networks, and the financial strength of a Saudi partner. Additionally, potential economies of scale can be leveraged through such a partnership.

Despite the clear advantages of forming a joint venture in Saudi Arabia, foreign investors should undertake thorough planning that focuses on financial, legal, and strategic aspects. This article provides a practical guide to the key considerations.

Foreign investors must familiarize themselves with the local tax and financial framework to optimize their chances of success. Contractual agreements with local partners should clearly regulate the following key points:

- Capital Contribution: The parties should clearly define what assets (e.g., cash, intellectual property, know-how) and in what amounts they contribute to the joint venture. A realistic valuation of the contributed tangible and intangible assets is required.

- Profit Distribution: It must be determined when, how often, and in what proportion the profits generated by the joint venture will be distributed to the partners.

- Loss Allocation: The parties should agree on how potential losses of the joint venture will be borne.

- Financing Arrangements: Various financing options should be considered to cover the joint venture’s operational and investment capital needs. These include shareholder loans as well as Sharia-compliant financing models such as .

- Tax Regulations: The tax obligations of the parties must be clearly defined. Foreign investors are subject to a corporate tax rate of 20%, while Saudi partners pay a Zakat levy of 2.5% on their net income. Foreign investors should also examine whether double taxation agreements (DTAs) provide benefits such as tax exemptions or deductions. Notably, Germany has not concluded a DTA with Saudi Arabia. Moreover, companies operating in newly established Special Economic Zones (SEZs) can benefit from significant tax advantages.

- Exit Strategies: It is advisable to include clear exit strategies in the contract. These may include clauses regarding the purchase or sale of shares, as well as valuation methods for situations where a party wishes to exit the joint venture.

Foreign investors should familiarize themselves with the relevant legal framework in Saudi Arabia. This includes Saudi corporate law, the Foreign Investment Law and its implementing regulations, the Arbitration Law and commercial courts, as well as labor law.

Legal Forms of Joint Ventures

Investors should understand the different corporate structures available for joint ventures:

- Limited Liability Company (LLC): The most common structure for joint ventures, offering a flexible framework and limited liability.

- Joint Stock Company (JSC): Often used for large projects and ventures requiring significant capital.

- Simplified Joint Stock Company (SJSC): A new structure combining elements of LLCs and JSCs, providing greater flexibility in corporate governance.

Foreign Investment Law

Foreign investors should be aware of the key provisions of Saudi Arabia’s investment law, which governs their business activities in the Kingdom. The most important aspects include:

- Approval by the Ministry of Investment (MISA): Every foreign investment must be approved by MISA, which acts as a one-stop-shop for all necessary formalities, from company registration to obtaining licenses and permits. Notably, the previous licensing system will soon be replaced by a registration system, with detailed regulations expected in February 2025.

- Liberalization of Investment Restrictions: Saudi Arabia has significantly eased foreign investment restrictions and now allows up to 100% foreign ownership in most sectors, except for strategic areas such as oil and gas, media, security, and defense, which remain restricted.

Why is ISIC4 Relevant?

The classification of investment activities under the International Standard Industrial Classification (ISIC), Version 4 (ISIC4), is a key consideration for foreign investors in Saudi Arabia. ISIC4 is an internationally recognized system for categorizing economic activities, developed by the United Nations.

Correct classification of an investment activity under ISIC4 is crucial, as it directly impacts approval and regulation by MISA. The choice of the appropriate classification affects:

- Approval Procedures: MISA uses ISIC4 as a reference for categorizing investment projects, but responsible officials are often not sufficiently familiar with the classification details. Incorrect classification can therefore lead to delays or unnecessary restrictions.

- Permitted Activities: Certain sectors are subject to regulatory restrictions or specific requirements. A precise ISIC4 classification helps avoid unclear or incorrect restrictions.

- Investment Incentives: Tax benefits and incentives often depend on correct industry classification. Choosing an ISIC4 category that best matches the joint venture’s business activity can provide financial advantages.

- Minimum Capital Requirements: The choice of ISIC4 classification can have direct implications on the required minimum capital. For example, an industrial license for a business activity involving production requires a minimum capitalization of SAR 1,000,000.

- Trade/Distribution Licenses: Any sales activity, whether following a production phase or through resale, may require a trade or distribution license with significant capital requirements (at least SAR 26,667,000 with Saudi participation and SAR 30 million for 100% foreign ownership). Therefore, classification under certain trade categories should be avoided if the goal is to minimize capital requirements.

- Service Categories: Activities classified under service categories generally require significantly lower capital requirements.

Strategic Considerations

- Understanding local business culture and etiquette is crucial for the success of a joint venture in Saudi Arabia. Personal relationships and trust-building play a central role in business interactions.

- Investors should conduct thorough due diligence on potential local partners, including financial audits and assessments of market reputation. Ensuring that both partners share similar business goals can prevent conflicts. A deep understanding of the business and social environment is essential to avoid misunderstandings or negative consequences arising from disregard for prevailing business, social, and religious norms.

Practical Tips

- Business agreements should be documented in a comprehensive joint venture contract and a detailed business plan that allows for flexible adaptation.

- A well-structured joint venture should include a Matrix of Authority, defining roles, responsibilities, and decision-making powers. Critical decisions should be classified as Reserved Matters, requiring the approval of all partners.

- Investors should establish robust licensing agreements to protect intellectual property when contributing technology or know-how to the joint venture. Confidentiality agreements and regular audits can provide additional security.

Compliance with Local Regulations

- Anti-Money Laundering & Anti-Corruption Laws: Investors must ensure compliance with Saudi regulations on money laundering and corruption by conducting due diligence and implementing internal compliance programs.

- Labor Law & Saudization Requirements: Foreign companies must comply with the Nitaqat system, which mandates quotas for employing Saudi nationals. Non-compliance can lead to sanctions or restrictions on work permits for foreign employees.

- Dispute Resolution: A dispute resolution clause is essential in joint venture agreements. Saudi arbitration law, based on the UNCITRAL model, provides an effective dispute resolution mechanism. The Riyadh Commercial Arbitration Center and the International Chamber of Commerce (ICC) are widely recognized arbitration institutions.

Conclusion

Setting up a joint venture in Saudi Arabia presents substantial business opportunities but requires careful financial, legal, and strategic planning. Foreign investors can maximise their success by understanding local regulations and cultural nuances. Partnering with experienced legal advisors familiar with Saudi laws and business practices is essential to navigate the complexity of the establishment process and ensure long-term success.

From Reporting to Governance and Risk Allocation

Environmental, Social and Governance (ESG) considerations are playing an increasingly influential role in how businesses operate, invest, and manage risk, especially within the European Union, where corporate sustainability and responsibility regulation have been on the agenda in recent years.

With the adoption of the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD), many companies anticipated a significant shift in compliance. Since then, the EU has introduced simplification measures to streamline reporting and due diligence obligations, reduce the administrative burden, and improve proportionality, particularly for small and medium-sized enterprises (SMEs), while maintaining the core sustainability objectives.

While opinions may differ regarding the evolution of environmental, social, and governance (ESG) in EU regulation and the subsequent postponements of reporting obligations, regulatory developments appear to have, in practice, supported a shift in perspective. Sustainability is no longer viewed solely as a reporting requirement, but increasingly as a matter of governance, strategy, and risk allocation. This development is welcome, as the regulatory framework’s underlying objective is to advance the green transition, which in turn requires a change in how companies integrate sustainability into their decision-making and operations.

This focus on sustainability influences businesses of all sizes, including SMEs. Even companies not directly subject to the CSRD or CSDDD anticipate that ESG requirements will be passed down through the supply chain. Many non-reporting SMEs are already embedding sustainability practices, and this trend is likely to continue. In other words, sustainability policies are already affecting companies well before any formal reporting obligations kick in.

Environmental, Social, and Governance in Contract Architecture

One of the key means of implementing environmental, social, and governance obligations and objectives in day-to-day business operations is through commercial contracts and the requirements and commitments embedded in them.

Even where a company itself is not directly subject to extensive reporting or due diligence obligations, corporate sustainability and responsibility expectations flow through the market via contractual relationships. Larger undertakings within the scope of CSRD and, in due course, the CSDDD require contractual assurances, information rights, and cooperation from their business partners, including SMEs operating within their supply chains. As a result, corporate sustainability and responsibility become a question of contractual architecture. Companies must consider not only price mechanisms, liability caps and termination triggers, but also how environmental, social and governance risks and obligations are addressed and allocated between the parties through legally enforceable contractual terms.

Translating Policies into Binding Obligations

A typical starting point is the incorporation of a code of conduct or sustainability policies into commercial contracts, often by reference and through an express obligation on the contracting party to comply with them. From a legal standpoint, this raises important drafting questions. Many codes are drafted as high-level public statements. When such policies are converted into contractual commitments, their wording, scope, and hierarchy relative to the main agreement require careful consideration. The obligations must be sufficiently clear to define the parties’ expectations, coherent with other contractual provisions, and proportionate to the commercial relationship. The obligations must also be capable of practical implementation and effective monitoring in the context of the agreement.

In practical terms, this may mean requiring the supplier to comply with specific labour standards, maintain documented environmental management procedures, report on emissions data, ensure traceability of key raw materials, or allow reasonable access for audits. Clearly defining what is expected, how compliance is demonstrated, and what consequences follow from non-compliance is essential for the clause to function effectively. Otherwise, clauses that appear comprehensive in theory and ambitious in scope may offer limited enforceability in practice, and their impact may remain marginal if compliance cannot be effectively monitored and verified. If policies are not properly translated into binding and operational obligations, the company risks a mismatch between what it promises publicly and what is actually required under its contracts. This may undermine consistency, weaken risk management, and expose the company to reputational and governance risks if its own stated principles cannot be enforced within its supply or distribution chain.

As part of this process, companies must also consider the protection of trade secrets and confidential information. For example, broad audit or data-reporting obligations may raise concerns about sensitive business information. Contractual terms should balance transparency with the need to protect legitimately proprietary data. Clauses such as confidentiality agreements or carve-outs for trade secrets can be used to ensure that sharing ESG-related information does not compromise confidential business information or competitive advantages.

Environmental, Social and Governance Clauses Across Different Contract Types

Besides codes of conduct and sustainability policies, environmental, social and governance-related clauses increasingly take more tailored and transaction-specific forms. In shareholder agreements, sustainability objectives may be reflected in governance structures or even linked to financial outcomes, for example by aligning dividend policies or incentive mechanisms with agreed climate targets. In employment contracts, obligations may extend beyond general compliance and include participation in corporate sustainability training programmes or adherence to internal sustainability guidelines as part of performance expectations.

In supply and manufacturing agreements, environmental, social and governance provisions may address traceability of raw materials, emissions reporting, waste management, energy efficiency standards or the right to replace a supplier if its environmental practices materially conflict with the contracting party’s sustainability commitments. Such contractual mechanisms increasingly affect SMEs operating as suppliers, as ESG expectations pass through the supply chain.

Construction contracts often include detailed requirements regarding material selection, lifecycle impacts, carbon footprint calculations and recycling or waste reduction procedures. For example, in Finland, legislation imposes low-carbon and energy efficiency requirements for new buildings, and a party undertaking a construction project is subject to mandatory reporting obligations relating to construction and demolition waste. These statutory requirements are typically reflected and implemented in the relevant project and construction contracts.

Across these different contract types, the practical significance is consistent. Environmental, social and governance considerations move from the level of general policy into legally enforceable obligations tailored to each specific legal relationship. Contracts function as a mechanism for allocating responsibility, managing compliance risk and aligning commercial incentives with sustainability objectives.

Proportionate Monitoring and Audit Rights

In the contractual implementation and monitoring of environmental, social and governance obligations, audit and information rights play a central role. They are closely linked to effective oversight and form an integral part of a coherent contractual framework. In practice, companies typically seek access to relevant data from their business partners and, where appropriate, establish inspection or audit rights to enable meaningful monitoring and verification, whether conducted directly by the company or, commonly, by an independent expert appointed for that purpose.

However, such arrangements must remain balanced. Overly burdensome provisions may needlessly disrupt day-to-day operations and reduce the willingness to cooperate, particularly for SMEs with limited administrative capacity. By contrast, well-designed mechanisms that balance transparency with confidentiality and operational feasibility are more defensible and more likely to function effectively in practice.

Contractual Remedies

As a general principle, the consequences of a breach are determined by the terms agreed between the parties. In practice, the parties will typically first seek to resolve the matter through discussion and good faith negotiations, allowing the non-compliant party an opportunity to clarify the situation and implement corrective actions within a reasonable timeframe. If negotiations do not lead to a resolution, it may be appropriate to proceed to stronger measures, such as contractual penalties, indemnification obligations, price adjustments, temporary suspension rights or other agreed sanctions, applied in light of the nature and severity of the breach.

The contract should clearly define what constitutes a breach, how it is assessed and what remedies are available in each scenario. Clear and proportionate step-by-step remedy structures enhance legal certainty, reduce the risk of disputes and ensure that material or repeated breaches may trigger more significant consequences, including termination where justified.

Strategic and Voluntary Environmental, Social and Governance Commitments

In the current EU landscape, implementing ESG considerations in commercial contracts is no longer simply a matter of reacting to directives. It is a broader exercise in risk management and corporate governance. Even as the implementation details of the directives may continue to evolve, market expectations, financing conditions and reputational considerations remain key drivers of sustainability integration.

In addition, some companies choose to position themselves as frontrunners in sustainability for strategic and reputational reasons. They may therefore incorporate voluntary environmental, social and governance mechanisms and requirements into their contracts that go beyond, or are not directly derived from, binding directives. By doing so, they signal to investors, customers and other stakeholders that sustainability is treated as a core business priority rather than merely a compliance obligation.

At the same time, it is important to recognise the practical limits of such commitments. Ambitious sustainability requirements may be more challenging for SMEs with limited financial and administrative resources. Meeting extensive reporting, certification or traceability standards can require investments in systems, personnel and external expertise. If contractual expectations are not calibrated to the size and capacity of the counterparty, they may limit the ability of SMEs to participate in certain supply chains. A balanced and proportionate approach helps ensure that sustainability objectives remain achievable and commercially workable across the contractual chain.

Conclusion

For legal practitioners, the central task is not to increase the number of environmental, social and governance clauses as such, but to ensure their quality, coherence and practical relevance. The objective is to design contractual mechanisms that are proportionate, enforceable and aligned with the company’s actual risk profile, industry context and sustainability priorities. Commercial contracts remain one of the most concrete tools for translating sustainability strategy into operational practice. Moreover, every contract lawyer should understand and apply key sustainability principles in their work, ensuring that ESG commitments become integral to legal advice and contract drafting.

The Strait of Hormuz is likely the most strategically important point for the global oil trade. In fact, approximately 20% of the world’s oil and gas passes through this narrow passage between the Gulf of Oman and the Persian Gulf every day.

Following the outbreak of war in the region, the impact on energy markets was almost immediate: oil prices quickly rose above $100 per barrel, and it is unclear how high they may climb in the coming weeks and months. As a result, transportation, production, and procurement costs are rising across industrial supply chains in many sectors.

For many companies engaged in international trade, this phenomenon creates a very real problem. Contracts signed months (or years) earlier—perhaps at a fixed price—must be fulfilled in a completely different economic context.

A manufacturer that sells goods for delivery in six or twelve months may find itself producing and shipping at much higher energy costs, while the price agreed upon with the customer remains unchanged.

This is a situation that recurs cyclically, for various reasons: from the COVID-19 pandemic to the subsequent raw materials crisis, and on to current geopolitical tensions.

When the increase in costs is so sudden and significant, a question inevitably arises: must the contract still be performed under the original terms, or is it possible to suspend or renegotiate the agreement to adapt it to the new circumstances?

The answer depends on several factors: first and foremost, on what the parties have (or have not) provided for in the contract, but also on the law applicable to the relationship and on the interpretation that judges or arbitrators may give to the rules in the event of a dispute.

Force Majeure and Hardship: Two Different Concepts

When extraordinary events occur—such as a war, an energy crisis, or the disruption of a trade route—many operators immediately invoke force majeure. However, in most cases, these situations fall instead under the category of hardship.

It is therefore essential to distinguish between these two situations.

When an Event Constitutes Force Majeure

Force majeure applies to cases where an extraordinary and unforeseeable event makes it impossible to perform the contract.

The characteristics of the grounds for exemption from liability depend on the law applicable to the commercial relationship, but generally require:

- unpredictability of the event;

- the event being beyond the affected party’s control;

- the impossibility of avoiding or overcoming the event through reasonable efforts.

Typical examples include:

- orders from authorities requiring the suspension of production

- embargoes or export bans

- logistical disruptions caused by war

In these situations, performance is not merely more costly: it becomes objectively impossible. The consequence is that the party unable to perform is generally exempt from liability for the duration of the event.

Hardship

The situation is different when performance of the contract remains possible but becomes economically much more burdensome.

The concept of hardship is generally based on four prerequisites:

- an event occurring after the conclusion of the contract

- unpredictability and extraordinary nature of the event

- a substantial alteration of the economic balance of the contract

- excessive burden of performance, but not impossibility

A sharp increase in the price of oil, gas, or other raw materials often falls into this category.

Goods can be produced and delivered, but doing so may entail costs far higher than those anticipated when the contract was signed.

The ripple effect along the international supply chain

In global industrial supply chains, the same goods are often the subject of a series of consecutive contracts.

The manufacturer sells to a trader, who sells to a processing company, which resells to an importer in another country, who in turn distributes the product to the end market.

When a hardship event occurs—such as a sharp rise in energy prices—the effect tends to ripple throughout the entire supply chain.

The first party affected by the cost increase will try to pass the increase on to its contractual counterpart, who, in turn, will find themselves in the same situation with the next link in the chain.

The risk is clear: one of the operators in the middle of the chain may face increased upstream costs without being able to pass them on downstream.

This is one of the most common problems in international supply chains.

What happens if there is no clause regarding price fluctuations

In commercial practice, it often happens that parties operate on the basis of orders and order confirmations without a formal written contract, or that a contract exists but contains no provisions regarding price fluctuations or hardship.

In such cases, when costs increase sharply, it is necessary to determine which law applies to individual sales contracts across the supply chain.

This can lead to very different situations:

- one law may allow for price revision or termination of the contract

- another law aplicable to a second contract may not provide for equivalent remedies

- a third contract may contain much more restrictive contractual clauses

The practical result is that an operator in the middle of the chain may face a price increase from their supplier without being able to pass it on to the customer.

A Common Legal Framework: The Vienna Convention on the International Sale of Goods (CISG)

Fortunately, many international sales contracts are governed by the 1980 Vienna Convention on the International Sale of Goods (CISG).

The convention has been ratified by 97 countries, including Italy and most major trading partners, such as the U.S., Canada, China, Germany, France, Spain, etc.

The central provision is Article 79, according to which a party is not liable for non-performance if it proves that the non-performance is due to an impediment:

- beyond its control

- unforeseeable at the time of the conclusion of the contract

- unavoidable or insurmountable

Traditionally, this provision has been applied to cases of force majeure.

In recent years, there has been debate over whether it can also be applied to cases of hardship, but international case law tends to be very cautious.

International case law on Hardship

Court decisions reflect a rather strict approach.

In some cases, even very significant increases in raw material costs have not been considered sufficient to modify or suspend the contract.

The reasoning is simple: those who operate professionally in international trade must take into account a certain degree of market volatility.

Only when the increase in costs exceeds an exceptional and unforeseeable level such as to radically alter the balance of the contract can hardship be invoked.

One of the most frequently cited cases is the Belgian Supreme Court’s decision in the Scafom case, which recognized the right to renegotiate the contract following a 70% increase in the price of steel.

However, such cases are relatively rare.

Generic clauses that serve no purpose

Many contracts contain hardship clauses copied from standard templates (boilerplate).

The problem is that these clauses often:

- list the effects of hardship

- but do not define when hardship actually occurs

The result is that, when prices rise, the parties may have very different opinions on what constitutes an “exceptional” increase and whether the event in question was “unforeseeable” or not.

The clause, therefore, does not resolve the issue, but defers it to discussion between the parties and, in the event of a failure to reach an agreement, to the courts or arbitrators.

What criteria can define a hardship situation

To make the clause truly effective, it is useful to establish objective parameters.

Among the most commonly used in international contracts:

- an increase or decrease in the price of a raw material beyond a certain threshold (±20% or ±30%)

- an increase in transportation or logistics costs within certain limits;

- significant fluctuations in the exchange rate beyond a specified range;

- the introduction of tariffs or trade restrictions

These parameters, linked to tolerance ranges, allow the parties to quickly and unambiguously identify a hardship event.

Remedies in the Event of Hardship

An effective clause should also address how to handle the situation.

The most common solutions are:

- renegotiation of the contract in good faith

- apply an automatic price adjustment

- appointment of an independent third-party expert to determine the new price

- temporary suspension of the contract

- right of withdrawal if no agreement is reached

These tools allow the parties to manage the crisis without resorting to litigation.

Audit of existing contracts: what to do now

At this point, the practical question becomes: how should we manage the issue in existing business relationships?

The first step is to conduct an audit of existing contracts with suppliers and customers.

1. Introduce comprehensive contracts in new relationships

If the relationships are governed solely by purchase orders and order confirmations, it is advisable to take this opportunity to draft comprehensive international sales contracts that include:

- a hardship clause

- warranty provisions

- remedies for breach

- limitations of liability

2. Update existing contracts

If the relationship is already governed by a contract, you should check whether a hardship clause exists.

If not, it may be useful to propose to the other party:

- a new contract, or

- a contract addendum dedicated to managing price fluctuations.

This helps prevent future conflicts and provides both parties with an effective tool to manage potential price shocks along the supply chain.

Conclusion

Commodity and energy crises demonstrate how exposed international contracts are to sudden changes in economic conditions. When a contract does not clearly address hardship management, the risk does not disappear; it simply shifts along the supply chain until it settles on the weakest link.

For this reason, companies operating within international supply chains should view the hardship clause as a strategic tool for managing contractual risk. A well-drafted contract does not eliminate market volatility, but it allows the parties to address it with clear rules, reducing uncertainty and preventing disputes.

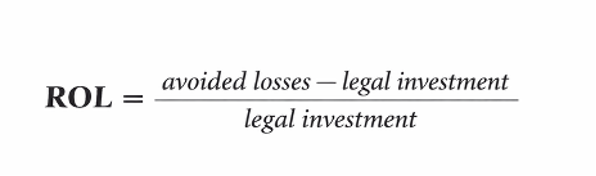

Summary: The challenge with preventive legal work is that it’s difficult to justify in the corporate budget—especially in organizations lacking a strong culture of risk prevention and mitigation. This article offers a practical solution: applying a “value-at-risk” approach helps leadership understand why every euro spent on preventive legal assessment can prevent multiple euros in litigation costs, sanctions, business disruption, and avoidable losses. A simple Return on Legal (ROL) metric makes that value tangible by calculating avoided costs from past disputes and modeling the financial effects of potential future lawsuits.

Why Legal Risk Management Needs a Financial Metric

Most companies already invest in preparedness—just not consistently in legal. They run security drills, insure assets, addres civil and product liability, test business continuity plans, and model financial risk. However, legal risk is often overlooked and, when considered, remains in the “qualitative” bucket: high/medium/low, red/amber/green, or a list of concerns in a memo.

That becomes a problem when decisions are made. Budgets are approved in numbers, not adjectives. If companies want legal preparedness to be funded like business preparedness, they need a framework that decision-makers are already familiar with. That’s where applying a value-at-risk approach helps.

Legal Risk as Value-at-Risk

Value-at-Risk in finance asks a simple question: how severe could the downside be, and how often might it happen? Legal risk can be approached in a similar way by considering two factors: the likelihood of an event (such as a claim, dispute, investigation, enforcement action, fine, lawsuit, or class action) and the impact if it occurs. Things can get very complicated, but for the sake of this article, a very simplified way to express it for a single- well defined, loss event might be:

“Total impact” is often underestimated when assessing legal risk. Direct legal costs are just one part of the picture. A dispute can consume leadership time, divert key teams from revenue-generating work, slow down delivery or product launches, damage supplier relationships, and cause customer hesitation. In other words, legal risk is often an operational risk with legal triggers.

Therefore, we should consider that legal risk rarely appears as a “fixed impact if it happens,” and the expected risk value often accumulates through the correlation of different factors. For example, one investigation can trigger follow-on lawsuits, a license can be revoked, a class-action can start, or enforcement can occur across multiple jurisdictions. If we want to account for this scenario (“how severe could the downside be and how frequently”), then the framework should involve a loss distribution over a period, which might look like this.

Expected legal loss (per period) = expected frequency x expected severity

This isn’t about finding the perfect formula. It’s about making legal exposure comparable to other risk areas where investment decisions are routinely supported with quantified downside.

Introducing Return on Legal (ROL)

Preventive legal work often goes unnoticed when it succeeds. When a contract dispute is avoided or a claim is settled early, there is no dramatic event—only the absence of damage. This is exactly why preventive advisory is often seen as a cost during budgeting: it appears more like an expense than an investment. A Return on Legal (ROL) metric addresses that gap by translating prevention into business results. In practical terms, ROL shows how much cost and disruption you save for every euro/dollar invested in legal risk assessment and prevention.

A definition could be expressed as follows:

When considering avoided losses, one should factor in a projection over a period of time (e.g., 3 years), the probability of a claim (e.g., 10%), and a baseline frequency of disputes. From there, it’s easy to get lost in complex calculations that take many variables into account; my point is not to achieve perfect precision but to make a credible, quantifiable estimate that supports better decisions in legal risk assessment and budgeting.

Measuring ROL: Retrospective vs. Forward-Looking

A convincing ROL approach combines what companies already know from experience with what can reasonably be modeled going forward.

First, there is the backward-looking perspective: assessing costs based on past litigation and disputes. Most companies have at least a few cases that can serve as reference points. The task is to identify where earlier legal intervention could have minimized the likelihood of escalation or the severity once a matter arose. This could be something as simple as improved clauses that prevent a dispute from escalating, earlier involvement of external counsel leading to quicker settlements on better terms, or custom dispute resolution clauses that reduce discovery burdens and strengthen the negotiating position.

To estimate backward-looking ROL without overclaiming, we can set a baseline for “what happened” or what usually occurs when that type of risk materializes without intervention. Then, compare that baseline with the results achievable when preventive measures are in place. There’s no need to pretend we can calculate the exact euro value to the last cent. What we require is a defensible range, based on actual costs (fees, settlement amounts, internal time) and business impacts that can be reasonably estimated (delayed launches, downtime, diverted capacity).

Second, there is the forward-looking perspective: forecasting the financial impact of potential future lawsuits. This is where the value-at-risk approach proves powerful. Decision makers identify the most relevant exposure types for their business and develop scenarios for each—typically best case, base case, and worst case—then assign probability ranges. The simulation becomes more meaningful when they consider how specific preventive measures influence the model. Some actions decrease probability (for example, compliance controls and training). Others lessen impact (such as better contracts, liability limitation clauses, response protocols).

Many do both. In the end, leadership gets a quantified story: this prevention program lowers expected annual legal losses and reduces exposure to litigation-related damages. This mirrors the decision-making approach used in other preparedness and risk-management programs.

Let’s make an example of how ROL works

Imagine a business line where disputes often come from contract ambiguity and inconsistent negotiation practices. In the past, the company occasionally faced lawsuits or arbitration, but more frequently it dealt with costly “pre-litigation” escalations that still took months and used up a lot of internal resources.

A preventive program—featuring updated templates, negotiation playbooks, and targeted training—incurs a clear cost. From a value-at-risk perspective, you compare that expense to the expected loss without the program over a certain period: not only external fees and settlements but also the estimated operational impact of ongoing disputes. If the program decreases how often disputes escalate and accelerates resolution times, the avoided losses can quickly outweigh the preventive costs. That difference reflects what ROL captures in a way that leadership can act on.

ROL Implementation: Keep It Lean and Actionable

ROL does not require a perfect dataset on day one. What it needs is consistent categorization, conservative assumptions, and a commitment to improve the model over time. A practical starting point is to gather three streams of information: historical disputes and their total costs; recurring risk hotspots (such as contracting patterns, product or market launches, HR issues, data/privacy exposure, supplier disputes, client disputes); and operational impact estimates that the business already uses in other contexts (like cost per hour of downtime, cost of delays, internal resource allocation).

A practical starting point is to pull together three streams of information:

- historical disputes and their total cost;

- recurring risk hotspots (contracting patterns, product or market launches, HR issues, data/privacy exposure, supplier disputes, clients disputes); and

- operational impact estimates that the business already uses in other contexts (cost per hour of downtime, cost of delays, internal resource allocation).

Where data is uncertain, ranges can be helpful. Managers can assign confidence levels and keep the model honest by using conservative estimates. Over time, the ROL model becomes more accurate as the company consistently tracks legal events and as prevention initiatives develop. The most important mindset shift is to treat legal as you would other risk functions: as a measurable way to minimize downside, not just a reactive cost center.

Turning ROL Into a Decision Tool

Once legal risk exposure can be expressed in value-at-risk terms, companies can prioritize legal work using the same logic as other investments: risk reduction per euro spent. This shifts the conversation from “Should we spend on prevention?” to “Where do we get the biggest reduction in expected loss and tail risk?” ROL also improves alignment with business teams. Instead of speaking in purely legal categories, it is possible to connect legal work to operational outcomes—fewer delays, fewer escalations, faster resolution, reduced management distraction, greater predictability in commercial relationships. Over time, this fosters a healthier operating rhythm: legal risk reviews transition from being ad hoc to becoming a routine part of preparedness, similar to finance risk reviews or security protocols assessments.

Conclusion

Applying a value-at-risk perspective to preparedness reveals legal risk in the language corporate leadership already uses to allocate resources. A Return on Legal (ROL) metric then makes preventive legal advice concrete by turning avoided costs and operational losses into measurable value. By combining evidence from past disputes with future-focused simulations of potential lawsuits, companies can build a credible, data-driven argument that every euro invested in legal risk assessment can prevent multiple euros in losses—and that prevention is not just a “nice to have,” but a vital part of operational resilience.

How do you approach negotiating a trade agreement with China?

Based on my experience, let’s examine the issues to be addressed and the main questions to ask, taking the negotiation of a trade distribution agreement as a practical example.

Let’s start with the first issue that is important to clarify.

Nice Business Card – But Who Is This Guy?

Business cards, websites, printed or digital brochures, presentations, and any other materials shared in English have no official value in China.

The company name of the counterparty and the first and last names of people representing it or acting on its behalf, written in English, are only fictitious names.

To be certain of the company’s data and the identity of the persons, it is necessary to ask for the information in Chinese, with particular reference to the company’s business license (equivalent to the Companies House or Chamber of Commerce’s excerpt), from which the name, corporate purpose, registered and paid-up share capital, and the name of the legal representative can be inferred.

The data can then be verified by accessing the portal of the State Administration of Industry and Commerce (SAIC) of the province where the Chinese party is based.

This first verification is essential to ensure that you do not waste time or even run into scams (here’s an in-depth article on Legalmondo’s blog).

If You Don’t Own Your Trademark, Someone Else Will – and Charge You for It

Trademark First, Trade Later. China operates on a first-to-file system for trademarks, which means that the first person or company to register a trademark – not necessarily the original creator or most famous user – gains the legal rights to it. This creates a serious risk: if you haven’t registered your trademark in China, someone else might do it before you, and then either use it freely or demand a hefty ransom to give it back. Even high-profile figures like Elon Musk and Michael Jordan have been entangled in costly and protracted disputes with Chinese trademark squatters. In many cases, getting the mark back is highly complicated, and sometimes legally impossible.

To avoid this, register your trademarks early, even before entering the Chinese market. File directly with the China Trademark Office (CTMO) and don’t stop at the English version — consider registering a Chinese character version as well, since that is how your brand will often be known locally.

Once that base is covered, clearly state in your contract that your Chinese partner is not allowed to file a registration of any of your trademarks in China, in Latin or Chinese characters, and that he will use trademarks and IP rights in strict conformance to the contract and your instructions.

For a deeper dive into how to effectively protect your IP rights in China, check out our detailed article on the Legalmondo blog.

Contracts can wait. First, get on the same page

When negotiating with a Chinese partner, it’s often a mistake to begin the conversation by exchanging contract drafts. Instead, focus first on the substance — the relationship’s commercial and technical terms. Using a clear checklist of key discussion points (such as products, pricing, delivery terms, technical standards, after-sales support, exclusivity, duration, payment terms, etc.) helps ensure that both sides are aligned on what really matters. Take detailed notes and keep minutes of the discussions, especially where and when consensus is reached, and make sure those minutes are circulated and expressly agreed upon. Once substantial agreement has been achieved on the main terms, this memo can then be handed over to your lawyer, who will translate the business understanding into clear and coherent contractual language. This approach saves tons of time, as it helps avoid unnecessary back-and-forth on legal language before the core deal is in place.

Think Your NDA Covers You in China? Think Again

Yes, they are—and often underestimated. A well-drafted Non-Disclosure Agreement (NDA) is essential when the parties plan to exchange confidential information, such as technological know-how, commercial strategies, supplier data, or client lists. Especially in the early phases of negotiation or cooperation, before a main contract is signed, an NDA helps protect intellectual and business assets.

However, as with all contracts in China, a generic NDA template copied from other jurisdictions will likely be of limited use. To be truly effective, the NDA must be adapted to the specifics of the Chinese legal environment. This includes ensuring that it is enforceable in China: the NDA should include the proper dispute resolution mechanism (see below on why you should consider applying Chinese law and litigating in China), and it must specify clear, valid, and proportionate penalties for breach. In Chinese practice, stating specific contractual penalties (liquidated damages) is often more effective than vague references to compensation, as courts and arbitrators in China tend to enforce these more reliably if they are reasonable.

While a good NDA is useful, it often falls short in China’s manufacturing and sourcing landscape. This is where the NNN Agreement – standing for Non-Disclosure, Non-Use, and Non-Circumvention – becomes critical. Unlike standard NDAs that primarily focus on confidentiality, an NNN Agreement is designed to address the unique risks of doing business in China. It prevents the recipient from not only disclosing confidential information but also from using it for their benefit or bypassing the disclosing party to work directly with suppliers, clients, or partners. Which, in China, is a very real risk.

This broader scope is vital when dealing with Chinese manufacturers or intermediaries, who may otherwise be tempted to replicate products or contact customers directly or through third parties. As seen with the NDA, also the NNN Agreement must be drafted in Chinese, governed by Chinese law, and enforceable in Chinese courts -otherwise, it may offer little real protection.

Joint venture? Easy, Cowboy

A joint venture is often the first proposal that comes up when negotiating with a potential Chinese partner. It seems appealing: sharing risks and investments, accessing the local market with an ally, leveraging their knowledge and network of contacts. But the reality is often very different from what it appears to be.

A joint venture is a complex, expensive, and rigid corporate structure that requires significant investments of money, time, and human resources, as well as the ability to continuously manage often divergent interests among the partners. The vast majority of Sino-Foreign JVs have gone wrong, or will go wrong. Or very wrong. First and foremost, because the JV is usually managed by the Chinese partner, and exercising effective control over the company’s operations is a very challenging undertaking.

Before going down this road, it is essential to ask yourself a few questions: Is the joint venture really indispensable for developing this business in China? (Spoiler: generally, no). Are there less restrictive and risky alternatives, such as a distribution agreement or a licensing agreement? (Yes, almost always). And above all: how well do we really know our potential partner?

A joint venture should only be considered if it is strictly necessary for the project’s development, after carefully verifying the commercial viability and the reliability of the Chinese partner, and ensuring the ability to maintain effective control over the JV’s operations.

It is better to start with simpler and more flexible forms of collaboration to test the market and the relationship with the other party before committing to such a demanding investment. Otherwise, the mirage of the joint venture risks turning into a nightmare that can be very costly.

Memorandum of Understanding: Where Good Intentions Become Bad Contracts

A Memorandum of Understanding (MoU) is a helpful tool at the early stage of a commercial relationship. It serves as a roadmap for future negotiations, where the parties outline the main principles and intentions that will guide the drafting of the final agreements. When used correctly, an MoU can significantly facilitate negotiations by ensuring that both sides commit to negotiating the agreement in good faith and share a common understanding of key points such as pricing models, territorial scope, exclusivity, milestones, budget, or performance expectations.

However, an MoU must be used for what it is: a preparatory document, not a binding contract. Care must be taken to avoid ambiguity and unintended commitments. The text should clearly specify that the parties remain free to conclude – or not – the final agreements and which clauses are non-binding – such as the commercial framework or indicative timelines – and which provisions are binding, typically confidentiality, exclusivity during the negotiations (if agreed), governing law, and dispute resolution. A poorly drafted MoU, which includes overly precise and complete terms, can be misinterpreted as a final agreement, creating unnecessary legal risk. So yes, MoUs are valuable – but only when used correctly. If you’d like to know more, go deeper by reading this article.

Bad Drafts, Big Headaches, Poor results

Draft agreements used in China are often copied and pasted from incomplete, superficial, poorly organised templates written in bad English, which often do not match the Chinese version of the contract.

Correcting and integrating these drafts is complicated and more time-consuming than starting from a good template, with suboptimal results.

It would be better to propose a consistently constructed text and ask the other party to propose any changes and additions to this draft.

Your Western Contract Template Won’t Work Here

Even if an English-language contract is perfectly valid, there are many reasons why using contract templates built for other countries in the Chinese market is inadvisable.

The first is the fact that Anglo-Saxon-based agreements, such as those for the U.S., refer to a common law system (which is based on judicial decisions and case law precedents) that is very different from that of civil law countries (such as China and Italy), which derives from the Roman legal tradition, based on a codified set of written laws.

It follows that the layout of an agreement on the Anglo-Saxon model is different, much more detailed, and wordy than that of a typical agreement based on a civil law system. Since contract negotiations in China are generally lengthy and complex, working on redundant and complicated text at the outset does not help.

If we stick to the example of a distribution contract, it should be added that it is advisable to apply Chinese law to provide for arbitration based in China (e.g., at CIETAC) or in Hong Kong or Singapore (third countries, where, however, the costs of the procedure increase significantly) as the mode of dispute resolution. So, the contract should be built on a model that conforms to the law that will apply to the relationship.

Home Court Advantage Won’t Help You in China. In fact, quite the opposite

This is a typical point of disagreement in the negotiation of an international contract: the parties aim to have the law of their own country apply, and to stipulate that any disputes be adjudicated by their domestic courts.

In our case, insisting on the application of Italian (or any other foreign) law and state court is not a good idea: it should be considered, in fact, that a distribution agreement is carried out, for the vast majority, in the country where the distributor operates and where the products are sold (in our case, in mainland China).

In disputes, the parties’ (particularly the manufacturer’s) interest is to obtain a quick decision by the adjudicating body, especially if situations requiring immediate protection (such as unfair conduct or counterfeiting of trademarks and patents by the distributor) are ongoing.

None of this is possible if one goes to an Italian judge (with lengthy litigation time and the need then for a complex and costly process to recognise and enforce the decision in China); on the contrary, an arbitration in China, applying Chinese law, allows one to reach a decision quickly (on average 6-9 months) and, if necessary, also to obtain urgent measures to stop any unfair conduct.

Chinese Law Isn’t a Black Box (If You Know What You’re Doing)

The lawyer assisting you should know it.

Therefore, it is not a leap in the dark, and one should not fear surprises.

In addition, it should be remembered that an agreement is primarily based on the covenants that the parties have written in the contract; therefore, if the contract has been well drafted, the rules to be applied are clear.

Finally, if we consider distribution agreements, keep in mind that they are a framework contract, within which a series of separate product sales contracts are concluded. If both countries are contracting parties to the 1980 Vienna Convention on the International Sale of Goods (CISG), then the uniform, clear, and balanced rules of the convention apply automatically, just don’t opt out!

One Contract, Two Languages

The contract is also valid in English only. However, it is undoubtedly advisable to draft a Chinese version with facing text.

This is for several reasons: first, it prevents the Chinese party from having to arrange for a translation of the text during negotiations for its own internal use (top managers often do not speak English), thus slowing down the various steps of negotiations.

Also, to ensure that the Chinese side fully understands the agreement’s content and to avert misunderstandings (real or instrumental) about the interpretation of certain covenants.

Finally, it should be borne in mind that if the contract were later to be used before a court or administrative authority in China, the only language admitted would be Chinese; for this reason, it is better to have already a text agreed and signed by the parties in Chinese as well, rather than having to prepare a unilateral translation later.

Sign. And chop

Does the contract need to bear the company’s official stamp? Yes, and this point is absolutely crucial. In China, a company’s official “chop” (the red-ink stamp) is equivalent to a signature and is conclusive proof that the person signing the contract has the authority to represent the company. A signature alone, even from someone with an important-sounding title, may not be sufficient if it is not accompanied by the official chop. Without it, the contract might later be challenged or even considered void. Before signing, always verify that the stamp used matches the one registered with the company’s business license or official corporate records, and ensure that the stamp is applied on every page or at least on the signature page, in line with local practice.

Don’t Let Your Contract Collect Dust

Things change fast, especially in China. New products are added, market conditions evolve, people leave the company, new competitors emerge on the horizon, and so on. Companies constantly adapt to the new conditions, and so must the contract.

Any change in the relationship should be formalized correctly. To avoid misunderstandings and disputes, it’s advisable to include an integration clause in the contract, specifying that any amendments or additions will only be valid if agreed in writing, signed by the parties’ authorized representatives, and annexed as an addendum to the original agreement.

It’s not enough to include this clause – you must follow it consistently. If things change, agreements reached verbally, through Wechat messages, and through email exchanges may make things complicated if they are not formalised adequately according to the procedure set out in the original contract.

If you’d like to go deeper, check out this article.

Cross-border merger and acquisition (M&A) transactions are carefully structured. Lawyers negotiate risk allocation, manage regulatory exposure, and draft documents designed to withstand scrutiny across multiple jurisdictions. On paper, many of these transactions are sound.

And yet a surprising number of deals struggle to deliver their expected value.

When that happens, the problem isn’t in the paperwork. It’s in the people: Do they believe in the deal?

Belief starts with communication. If people don’t understand the deal, the documents won’t save it.

What Lawyers See vs. What Everyone Else Feels

For lawyers, a transaction is all about managing risk. Disclosure is deliberate. Regulatory exposure is controlled. Words matter, and for good reason.

For everyone else, it feels different.